We are witnessing a lack of momentum in a weak upswing within a weakly uptrending transitional market.

A relatively hard-money environment with very selective breakouts surviving. Watchlist feedback has worsened, with multiple squats & faded moves.

Conservative portfolios should keep holding relatively strong stocks with no (or minimal) open risk.

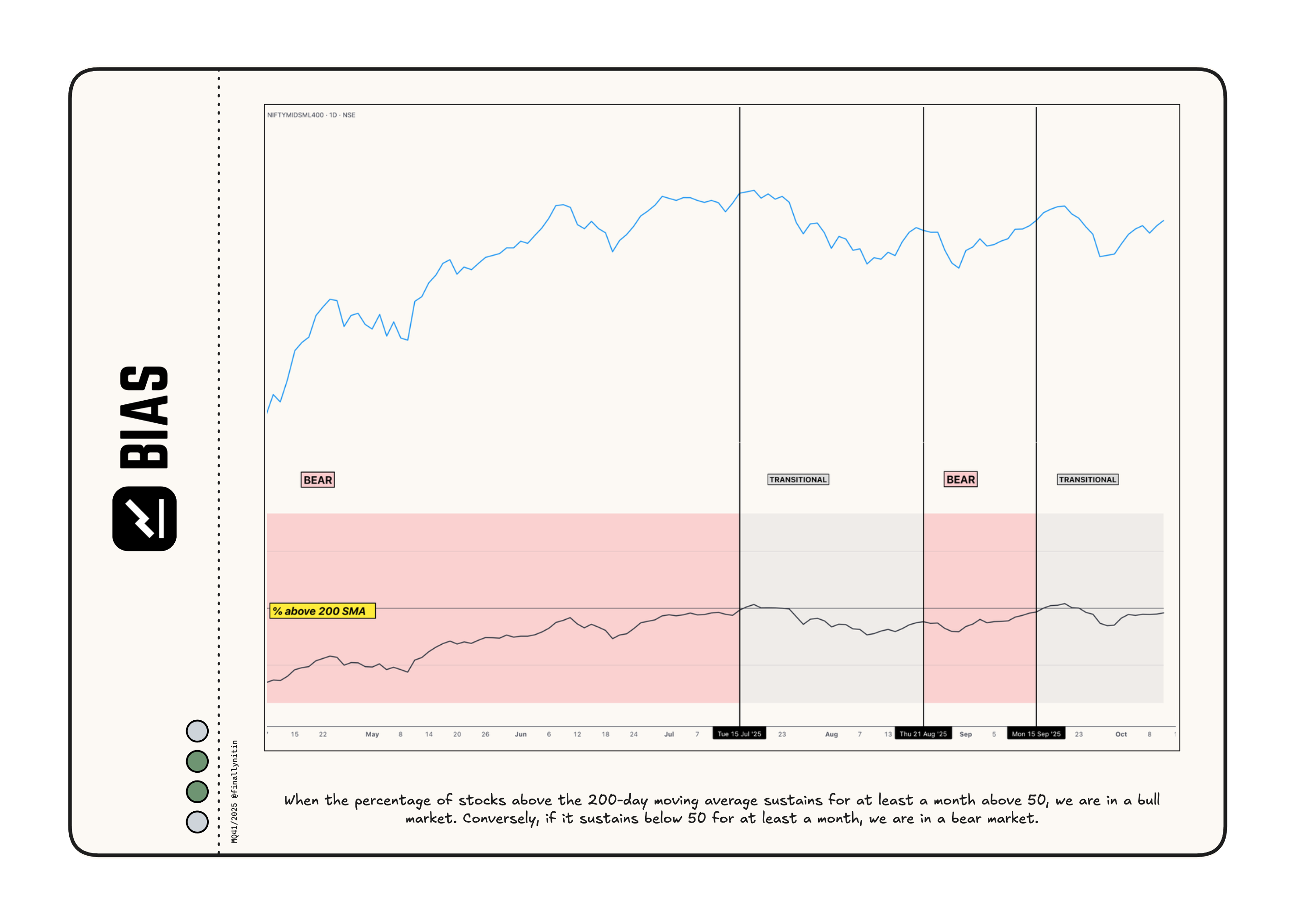

⦿ Bias: Transitional

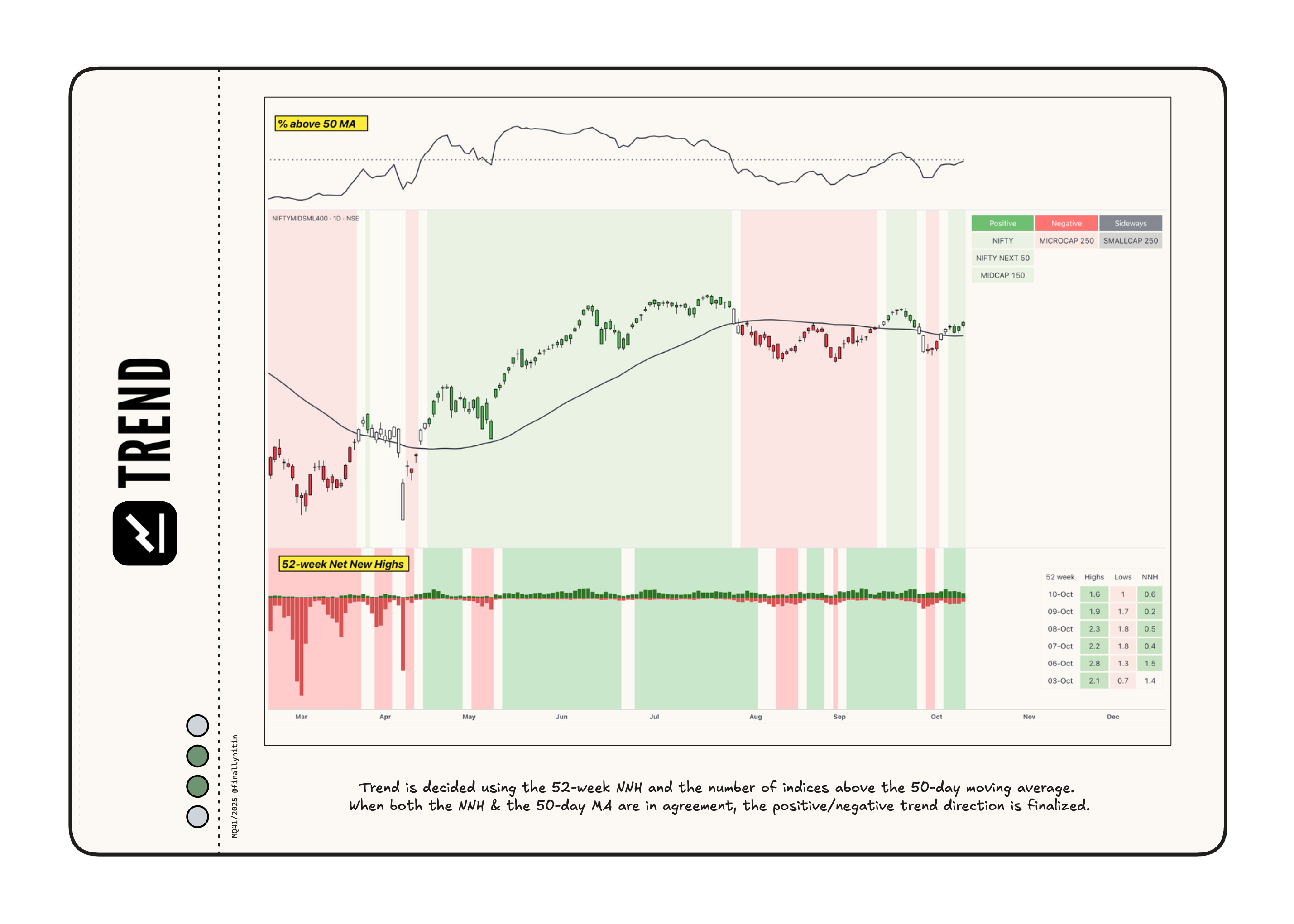

⦿ Trend: Uptrend (weak)

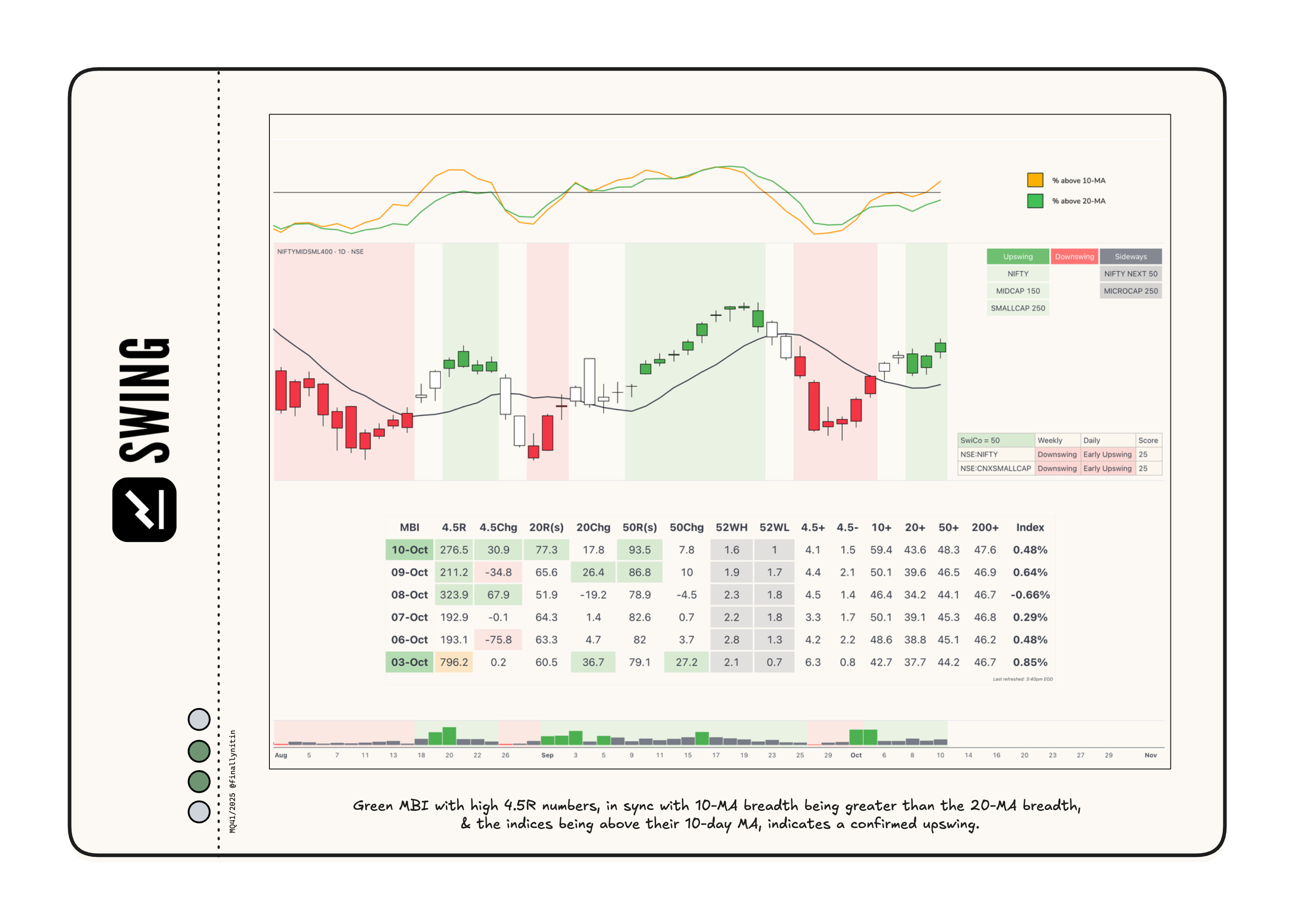

⦿ Swing: Upswing (weak)

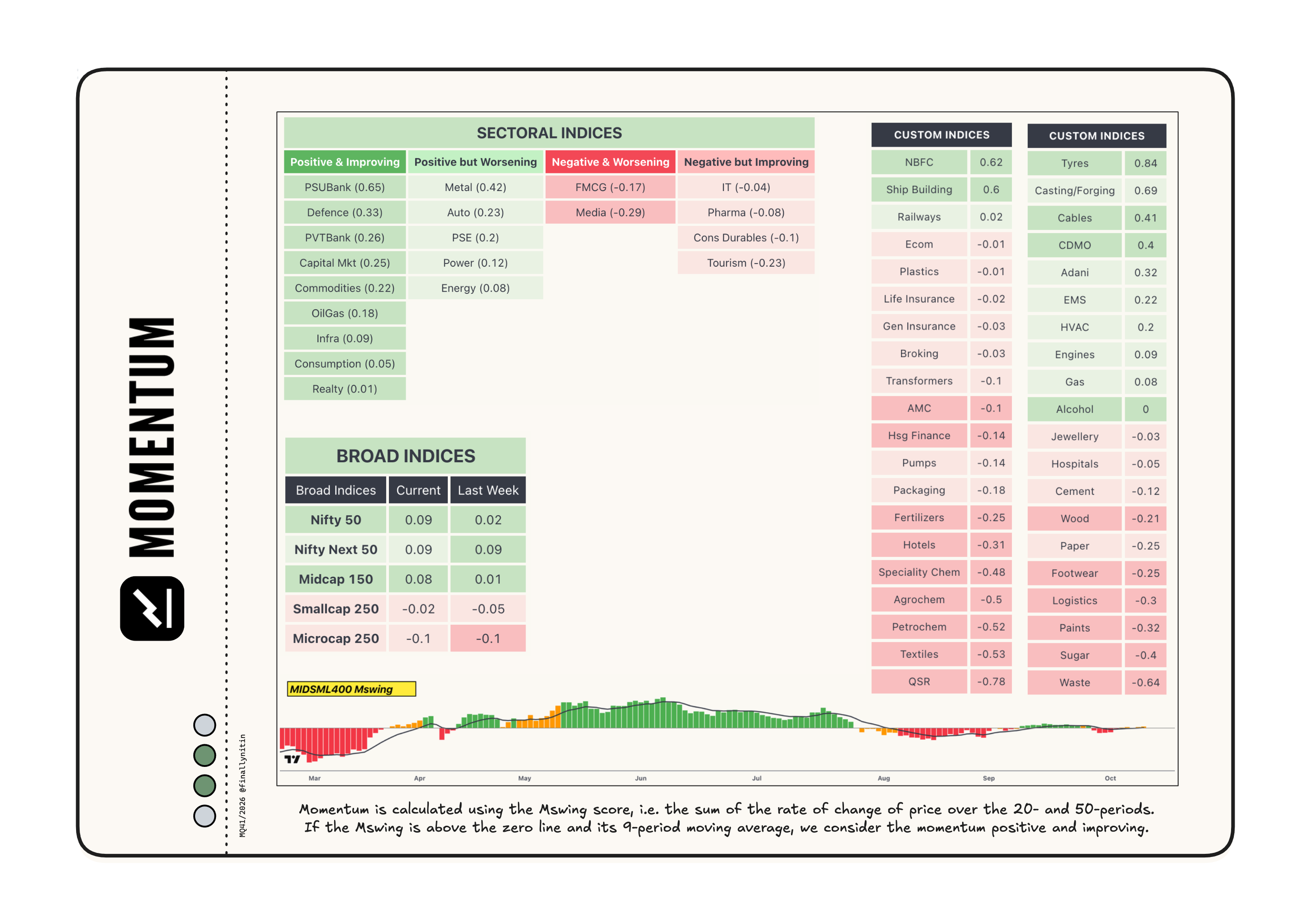

⦿ Momentum: Lacking

Bias → Transitional

From a long-term perspective, we are still in a transitional phase.

After staying below the 200-day simple moving average (SMA) for 7 weeks, more than 50% of the stocks moved up the 200 SMA three weeks back, and the market entered a bear-to-bull transitional phase. For the past 3 weeks, more than 50% of the stocks have stayed below their 200 SMA.

About 47% of stocks are positioned above their 200-day simple moving average. Although this is a minor improvement from last week, we remain below the 50% mark.

When the percentage of stocks above the 200-day SMA remains above 50 for at least a month, we will be in a bull market. If, instead, it stays below 50 for a month, we will return to a bear market.

Trend → Uptrend (weak)

After staying sideways for two weeks, the market is now in a weak uptrend.

52-week Net New Highs have remained consistently positive for the past three days. It’s worth noting that while the NNH values are positive, they have remained very low throughout the year. Hence, the trend, although an uptrend on paper, feels more like a sideways phase with not many stocks giving sustainable/tradable upmoves.

Over the past three days, major indices have not remained consistently above/below their 50-day moving averages, with approximately 48% of all stocks remaining above their 50-day moving averages.

The market will enter a confirmed uptrend if the 52-week highs consistently remain above the 52-week lows and more than 50% of stocks stay above their 50-day moving averages.

Swing → Upswing (weak)

The market is currently in a weak upswing.

After turning green last week, the MBI failed to produce even a single day with 400+ counts on the 4.5R.

Most broad indices remained consistently above their 10-day moving averages. Approximately 60% of stocks are trading above their 10-day moving averages, and, favoring the bulls, the 10% breadth has crossed above the 20% breadth.

Swing Confidence is 50, indicating that the portfolio can take half the maximum permissible open risk.

Momentum → Lacking

While most broad indices now have the momentum score above the zero line and its 9-period moving average, the momentum score’s value is only slightly positive, and hence, not much should be read into it. Henceforth, an Mswing value within +/- 0.1 shall be taken as a lack of momentum in either direction.

Many sectoral indices are exhibiting positive & improving momentum. PSUbank, Defence, PVTBank, and Capital markets have positive & improving momentum.

Shipbuilding, NBFC, Tyres, and Casting/forging are notable custom indices with positive momentum.

That’s all for this week. If you'd like to know when I publish something new, subscribe to my newsletter, and you'll receive the latest directly in your inbox.